Click image to open full size in new tab

Article Text

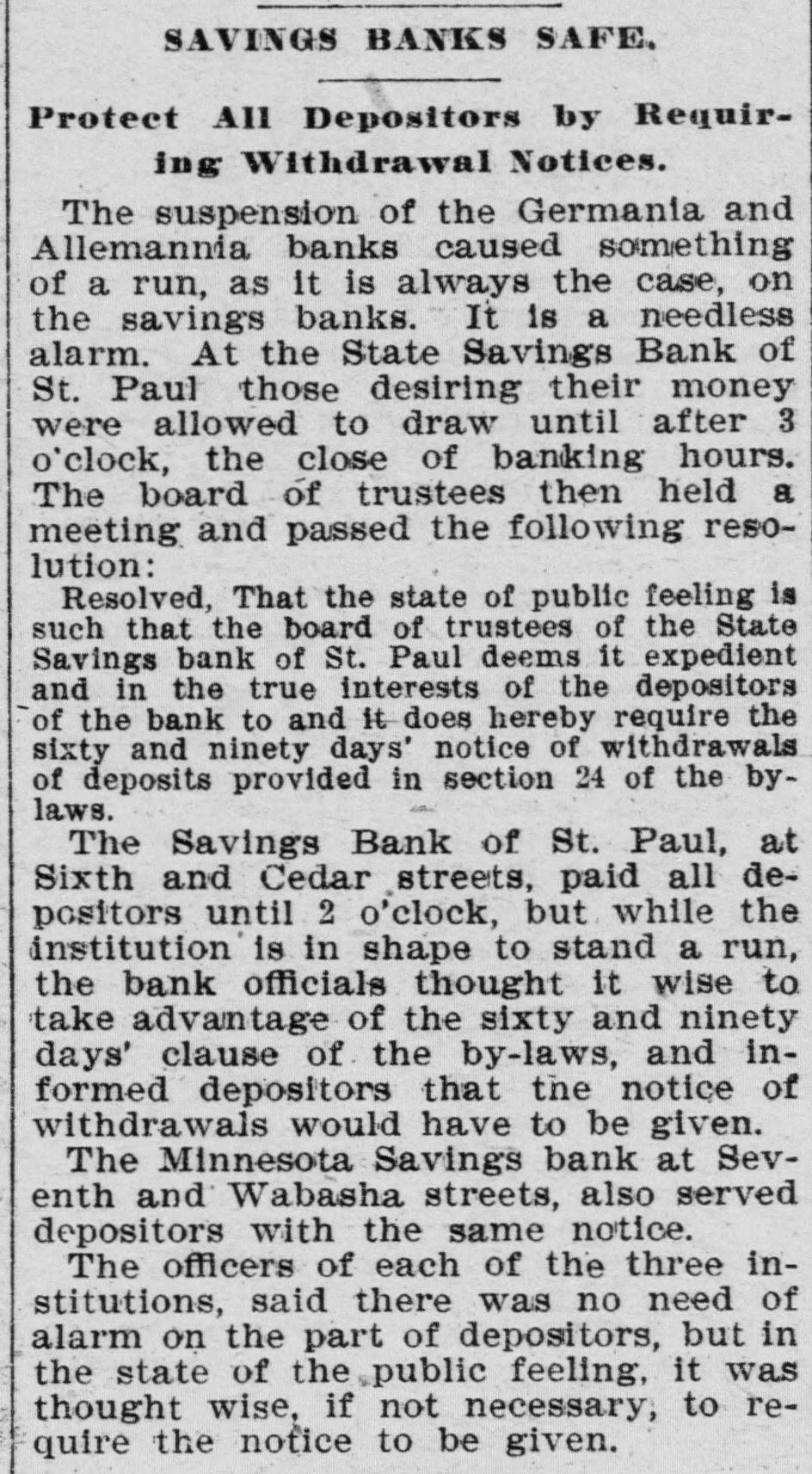

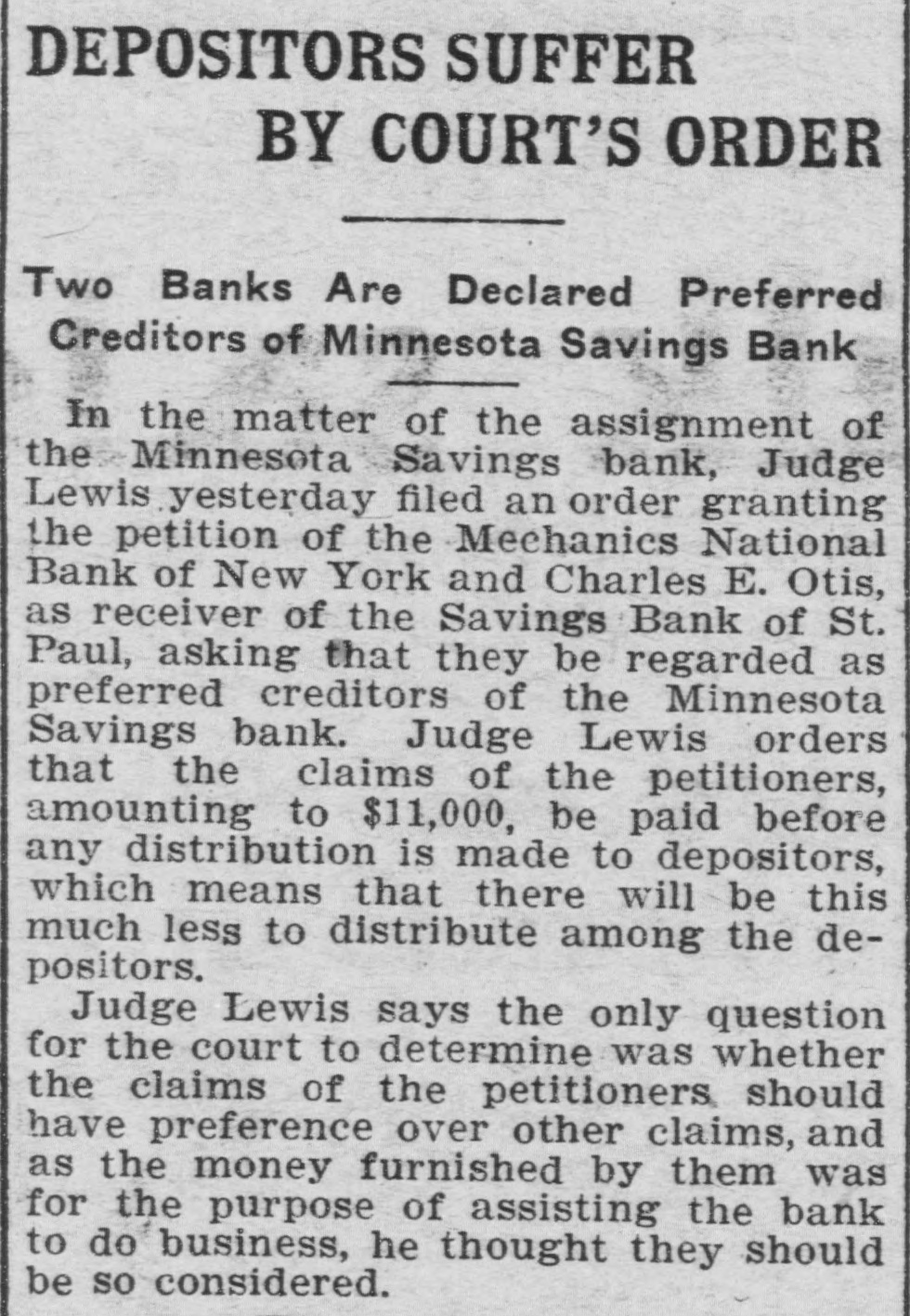

SAVINGS BANK OF ST. PAUL

## How the Appointment of a Receiver Can Be Avoided.

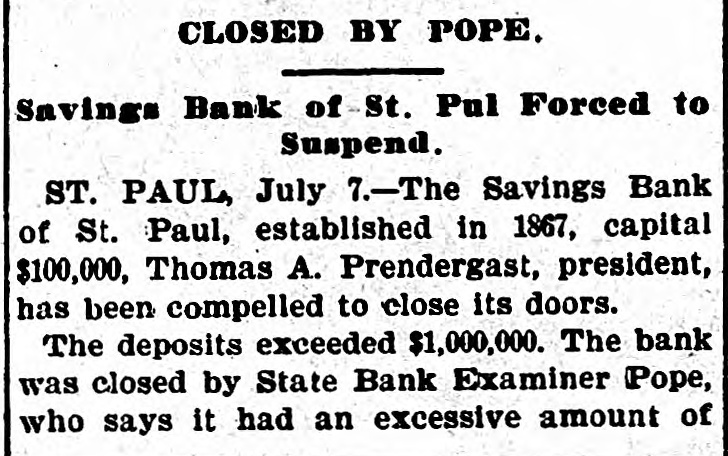

Three hundred depositors of the Savings Bank of St. Paul met in the senate chamber at the capitol last night and listened to a report of the general committee appointed to investigate the bank's affairs. J. J. Egan presided and opened the meeting with a review of the action taken by the depositors at different times since the failure. Little business was done and the reports submitted were not complete, as the committee had found that their time was too short to prepare a full statement. Arrangements were made for a meeting on the evening of Aug. 11, at which time printed summaries of the reports of the depositors and courts' committees will be distributed and detailed information given of the work of investigation.

The main interest of the meeting centered about the report of the committee appointed on July 9 to investigate the bank's books; real estate, commercial paper, tax certificates and other assets, with a view of presenting the depositors with an accurate statement of the affairs of the insolvent institution. As chairman of the committee, J. E. Stryker gave the following report.

"Your committee have found that in the time at their disposal they could not prepare more than a partial report. We have made considerable effort to get at the facts, but the magnitude of the undertaking prevented its completion before this meting. After considering the task before us the committee was divided into four subcommittees as follows: A committee to investigate the bank's real estate. A committee to examine the commercial paper of the institution not secured by real estate. A committee to look after the remaining items of assets, such as cash on hand, stocks and bonds and other matters.

The real estate committee found that owing to the number of pieces of real estate held by the bank, a thorough investigation would be impossible in the time at their disposal. They investigated partially, but are as yet unable to give a full report. Twelve different pieces of property were looked over and estimates made and these were compared with the estimates of the court's committee, which is engaged on the same work. The results were satisfactory. Of the other subcommittees, the one appointed to look after the bank's commercial paper found it difficult to complete their work and ask for additional time. The committee on tax certificates meets with the same difficulty, as it cannot readily secure necessary data.

The work of the committees, however, incomplete, has demonstrated, however, that the affairs of the bank are in such a condition that a receivership may be avoided with careful management. Present conditions are much more favorable than at first thought. Of the item of stocks and bonds it has been ascertained that the book figures, $93,000, are correct. This amount can be realized and the committee already has an offer to take the item for this amount. The gentleman who makes it will trust to the profits above this figure from the disposition of these assets as his commission. Of the commercial paper, the committee have been unable to complete a report. It is certain that this item will show some loss, how much cannot be said. There will also be some loss on the tax certificates. The committee has worked in conjunction with the committee of the court, which has gone through three-fourths of the real estate items, and would advise the depositors that its final report can be depended on for an exact statement of facts.

No one should become panicky yet. The showing so far is more favorable than anticipated. The committee especially advises against disposing of certificates of deposit to Minneapolis or other parties at a discount. If the depositors do not receive dollar for dollar they will obtain nearly that. Between two-thirds and three-fourths of the assets are contained in the items of real estate and real estate mortgages. Mr. Stryker was asked for an opinion as to what amount the commercial paper would bring. He replied that he was unable to express an opinion for the committee, but personally considered that it would be worth about $110,000.

Since the meeting held in Labor hall Judge Brill has granted the additional twenty-five days before taking final action, which was asked for by the depositors' committee. He has also instructed the court committee to file its report within five days of the expiration of the period in order to give the depositors time to review the report and make a statement before a depositors' meeting. M. R. Prendergast opened a short discussion with a suggestion to the stockholders that if any scheme of reorganization is effected a committee of depositors be appointed to place a valuation on all mortgaged property and all real estate owned by the bank.

"After this is done," he explained, "the depositors should be allowed to buy in real estate with their deposits and in this way utilize this item of assets. I would also suggest that since the depositors have been receiving 3 and 4 per cent on their money for the past few years they allow this committee to rebate this amount for two years and deduct it with the understanding that if the bank pays dollar for dollar they receive their interest before other claims are paid."

The only discussion out of the routine was occasioned by a motion of P. J. McDonald that before the next meeting, to be held Aug. 11, the depositors' committee prepare a printed statement of the report of the court committee for the use and information of the depositors. This raised a storm of criticism and was not clearly understood. C. W. Griggs restored order by explaining that a summarized report of the work of the court and depositors' committee would answer the purpose. A motion to the effect that such a statement be printed was carried.