Click image to open full size in new tab

Article Text

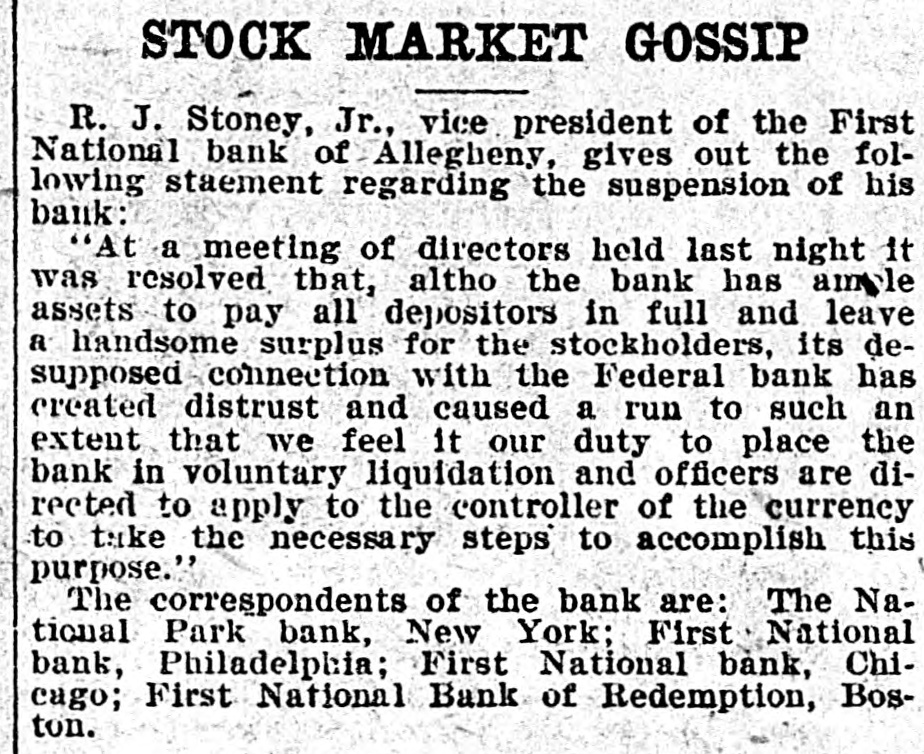

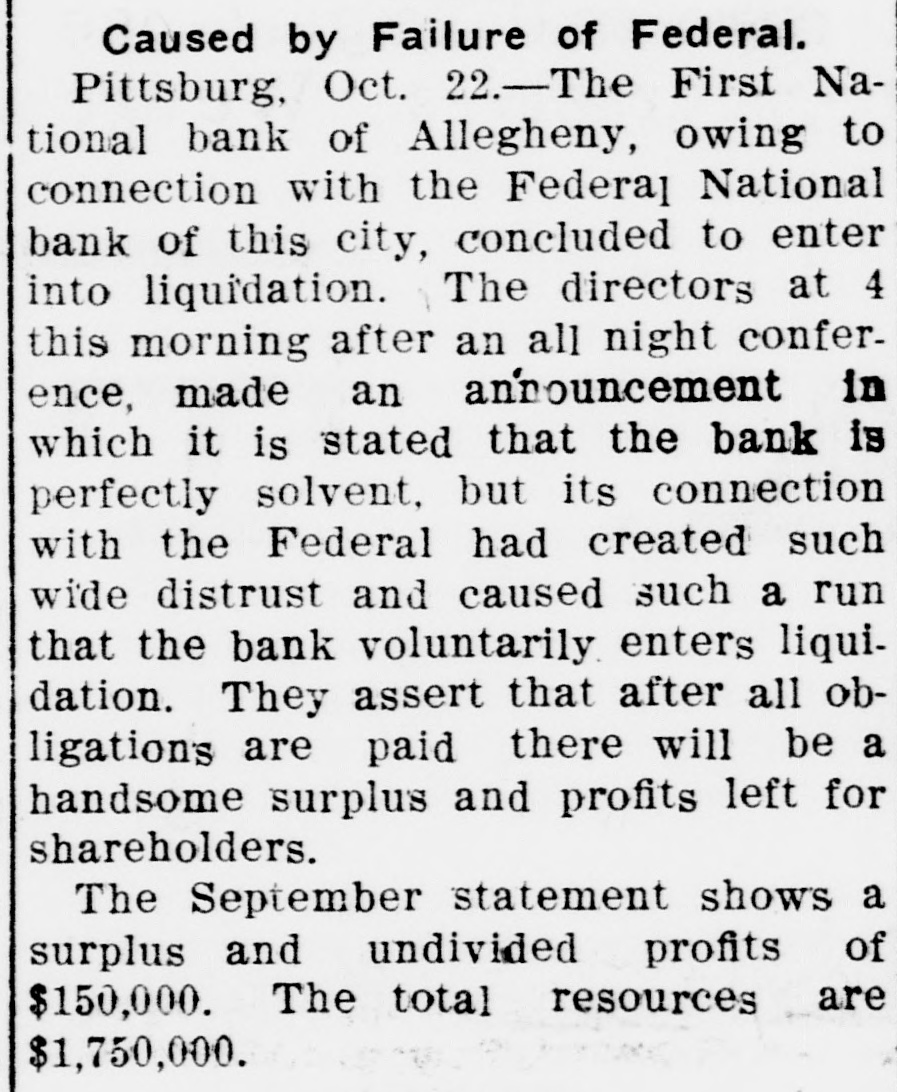

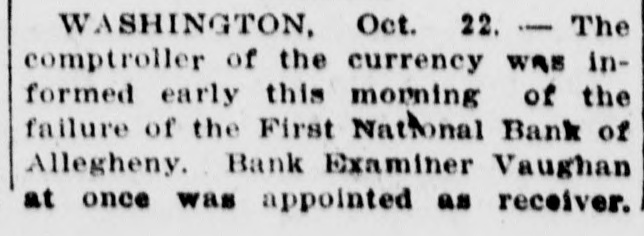

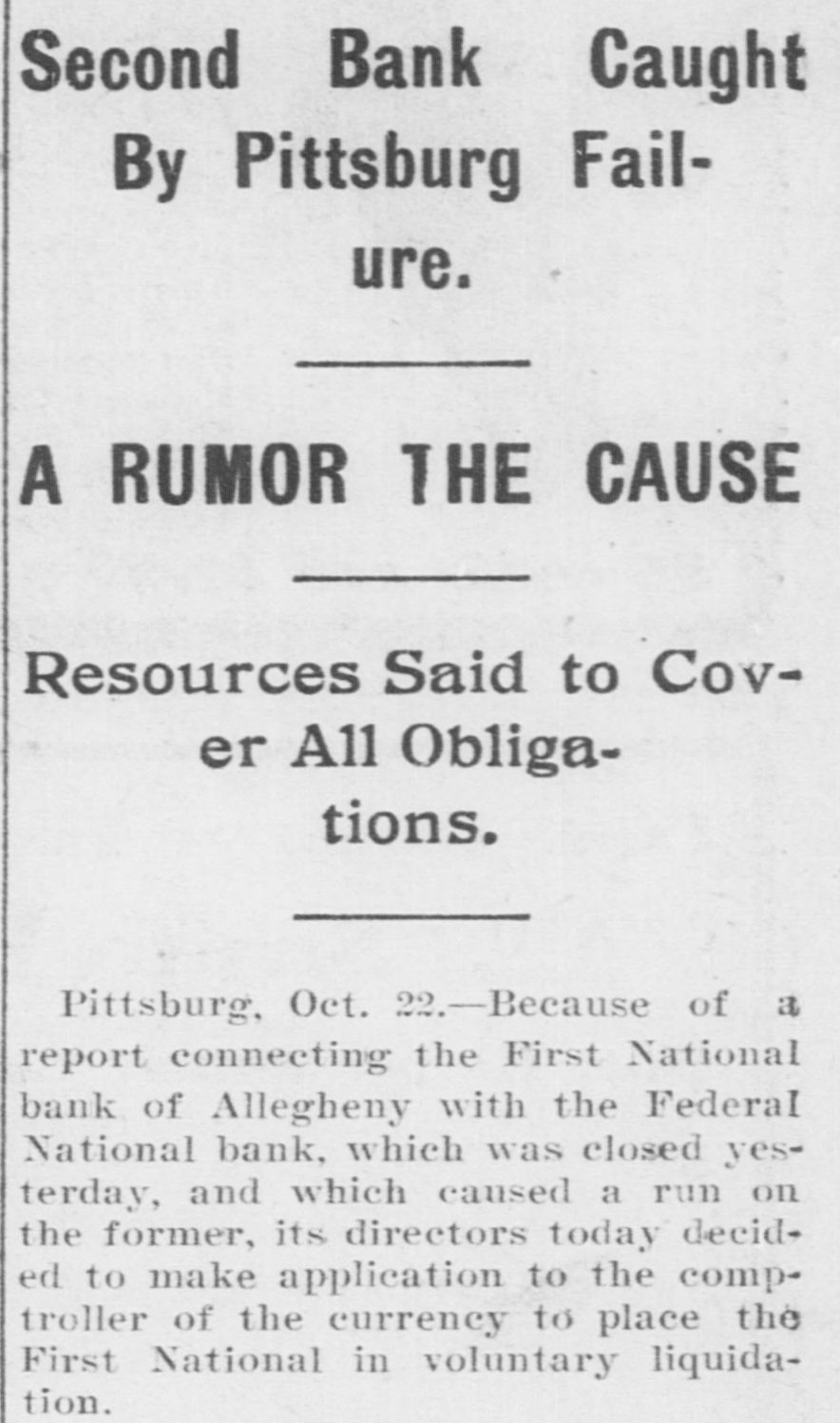

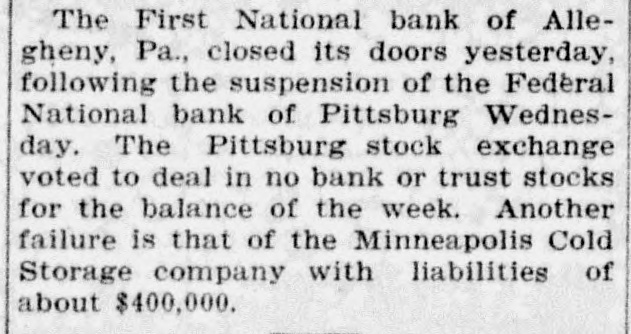

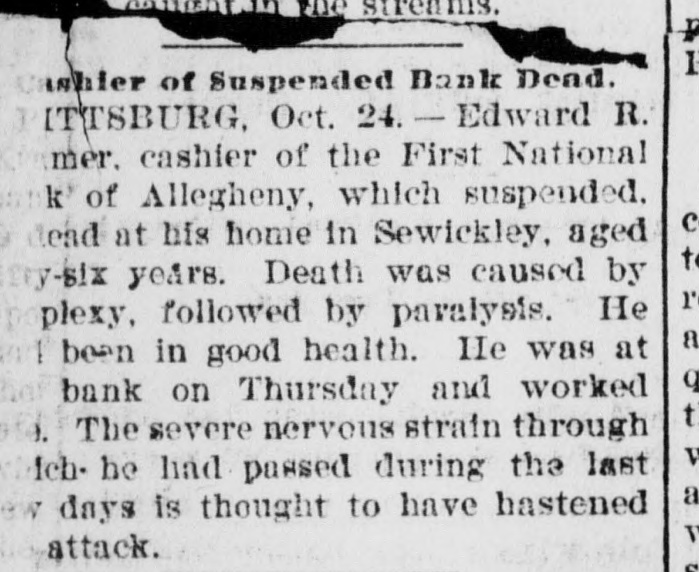

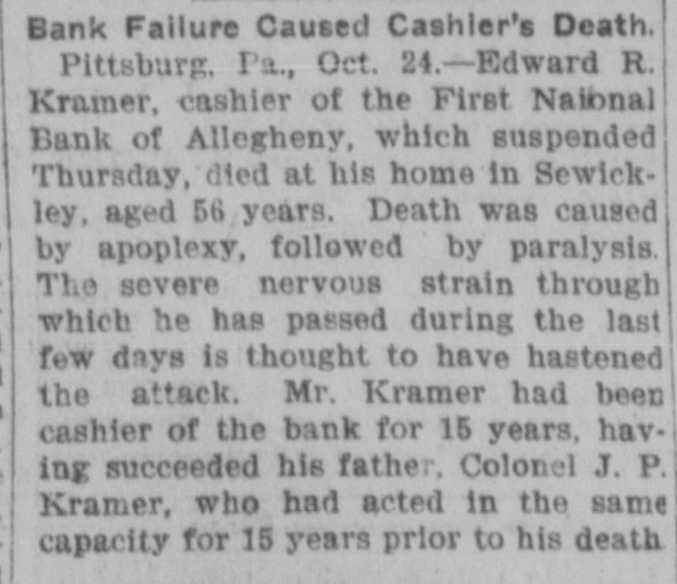

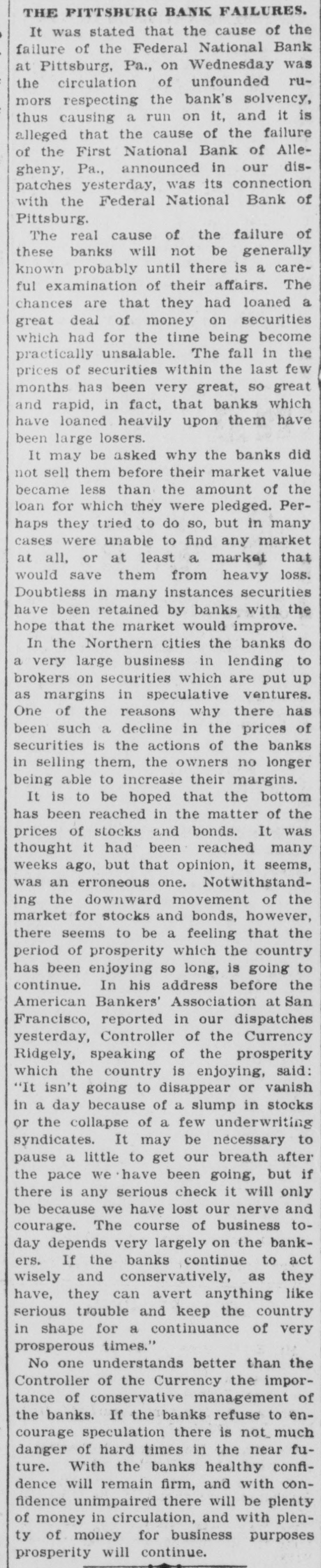

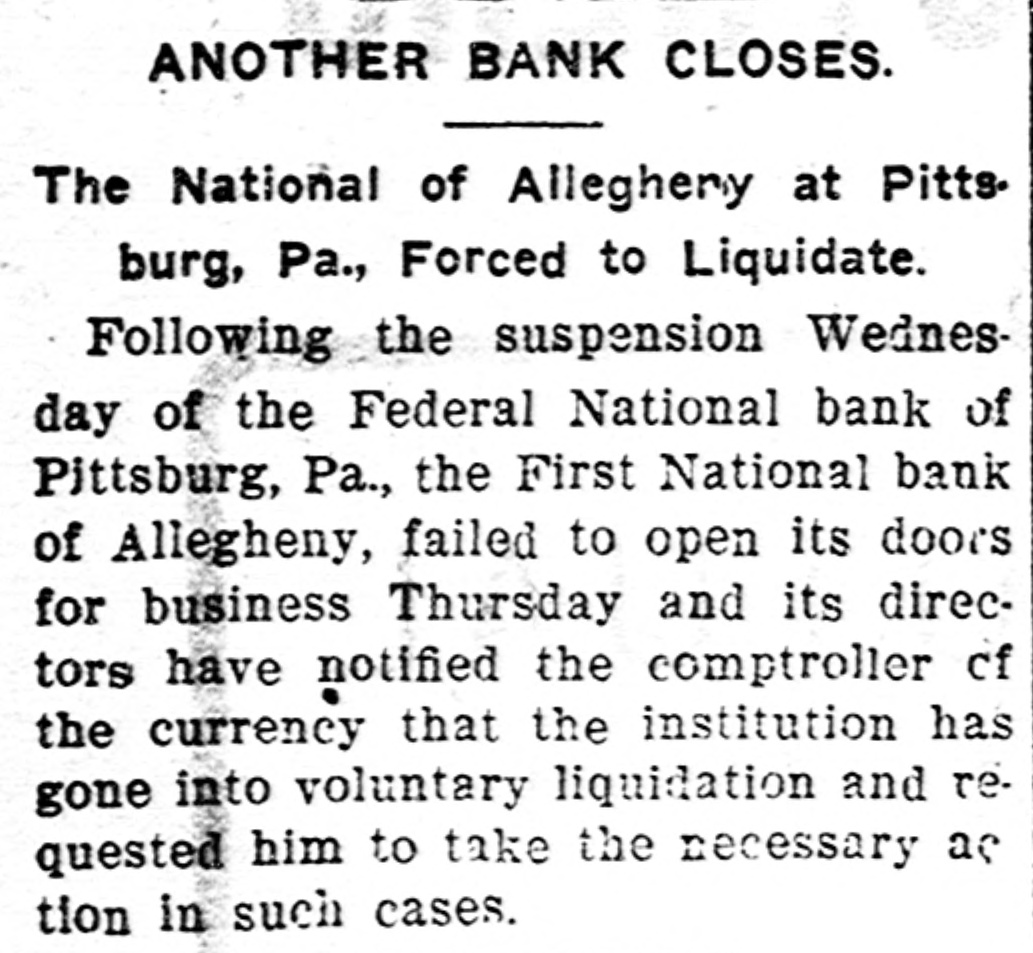

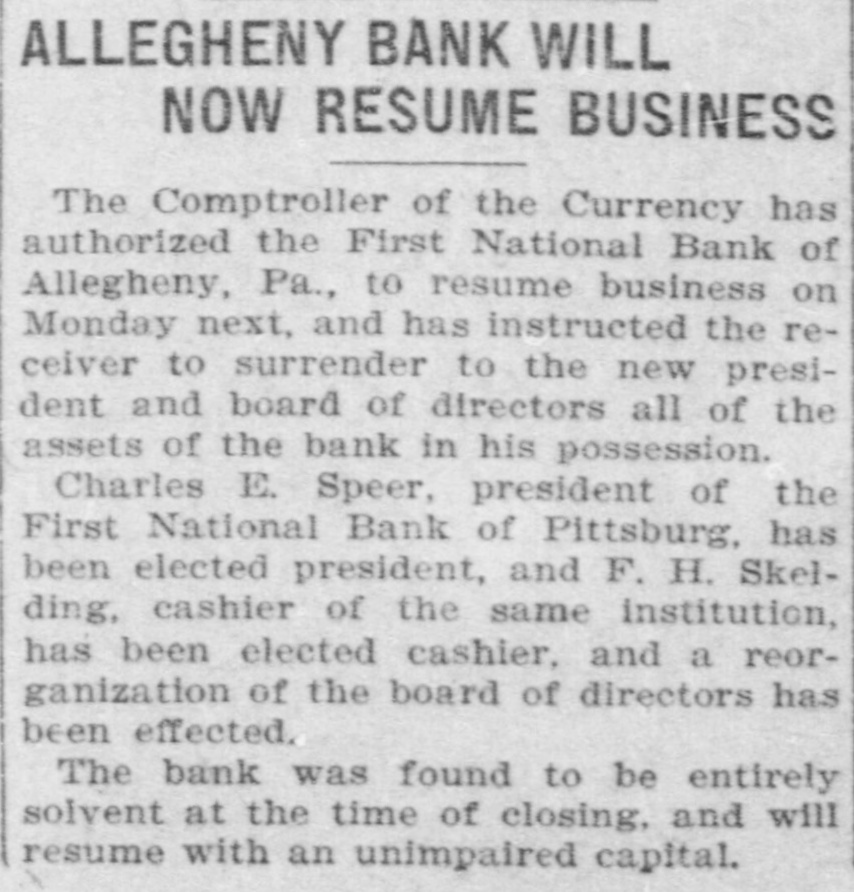

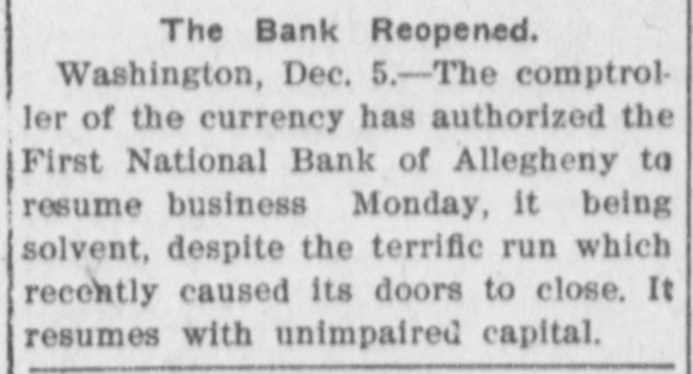

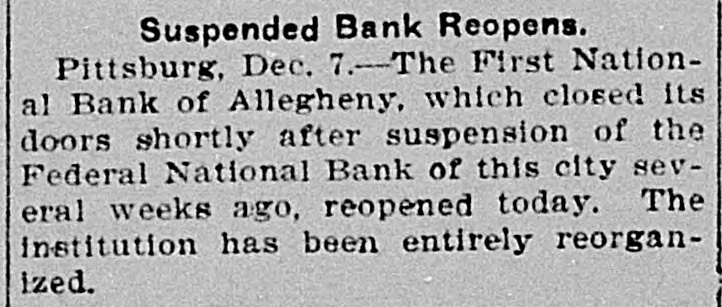

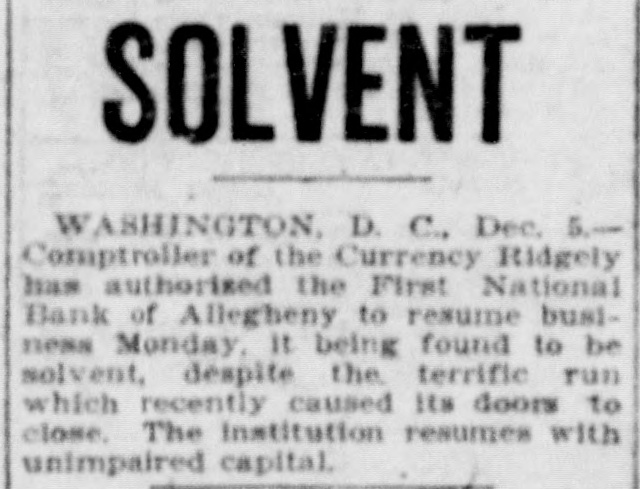

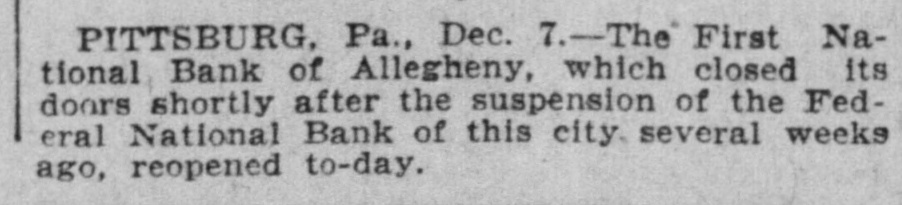

FINANCIAL AND COMMERCIAL THURSDAY, Oct. 22. The dominant feature of the stock market to-day was the demand for the investment issues. Evidences of a growing interest in securities of this grade have not been wanting of late and have been duly emphasized in this column. But to-day the dealings in bonds quite overshadowed operations in the stock market proper. All the established railway bonds were dealt in in good volume and at advancing prices, and, indeed, the prices of these bonds have already risen SO that the choice of bargains among them is by no means what it was even two weeks since. There is a natural order in operations of this kind which is almost invariably followed. The demand converges, at first, on issues of the very best character, first mortgage bonds of the well known railway lines yielding only a small return, but furnishing the very highest security, whose prices under almost all conditions fluctuate but little. It is obvious that a very small advance, comparatively, in the prices of bonds of this kind brings them to a point where their interest yield becomes sensibly diminished and where the prospective investor is inclined to turn from them to consideration of bonds which, although not quite SO well secured, are still thoroughly safe and afford a greater interest return. In time the supply of good bonds at suitable prices becomes exhausted and the buying spreads to preferred stocks, and so through the entire security list. Whether the investment of capital will proceed steadily along this path in the coming months cannot, of course, be said to be a settled question. It has, however, started on the journey after its accustomed fashion, and in the past its footsteps have rarely wavered from the beaten way. The combined strength and dulness of the stock market are, too, just what would naturally be expected under these circumstances. Bearish operators have discovered that there is no further liquidation by the general public upon the receipt of unfavorable news, a fact which usually indicates that these unfavorable developments were long ago foreseen and duly prepared for. Hence, while a "bull market" is by no means in order yet, and while any attempt of speculators to inaugurate such an affair would undoubtedly meet with disaster, prices of stocks stubbornly resist artificial attempts to depress them and in their own good time may be expected to display the effects of the general market convalescence. It seems to be clear that a very sharp line is now being drawn by all careful students and dispassionate observers of financial affairs between such events as the collapse of overboomed local enterprises in various cities, dragging down with them trust companies and other money lending institutions which have advanced funds upon forms of security for which there is little market, and the general business life of the whole country, especially that in the Western and Southwestern agricultural sections. It would be very singular if we had seen the last of suspensions, temporary or otherwise, of institutions of this character because of reasons like the foregoing. The important point for investors and speculators alike to remember is that such disasters as these-many of them of only small importance at best-are not of such a character as to involve sales of securities in Wall Street. While of course, they have a perceptibly greater bearing upon the general situation than the bursting of such incorporation bubbles in the industrial world as prevailed SO notably in 1899, the two phenomena are really kith and kin, and the wealth and prosperity of the country are such that far less harm to the business life of the country. as a whole, will be done by them than many people might suppose. Prices of stocks to-day closed very irregularly, most of the active issues, however, showing small advances. Among the railroad issues the Rock Island shares were especially strong, while in the industrial list a sharp break in Republic Iron and Steel preferred followed the announcement that a-number of the employees of the Republic Iron and Steel Company in Minnesota had been laid off. The decision of a local court in Montana awarding possession of the Minnie Healy mine to the Amalgamated Copper Company's chief antagonist, and restraining the Boston and Montana company from paying any dividends to the Amalgamated Company, but refusing to put the Boston and Montana company in the hands of a receiver, was really more favorable to the Amalgamated company than had been expected. Litigation over these matters, is of course merely in its preliminary stage and must pass through the higher courts before a final adjustment is reached. As the Amaigamated company has not been in receipt of the Boston and Montana dividends for some time, the preliminary decision to-day does not change the status of affairs in the least. The decision of the First National Bank of Allegheny, Pa., to go into voluntary liquidation, as a result of the suspension of the Federal National Bank of Pittsburg. with which it was allied, was considered as of little importance in Wall Street, because the solvent condition of the bank was perfectly realized. The one other important new development of the day was the declaration of an extra dividend of