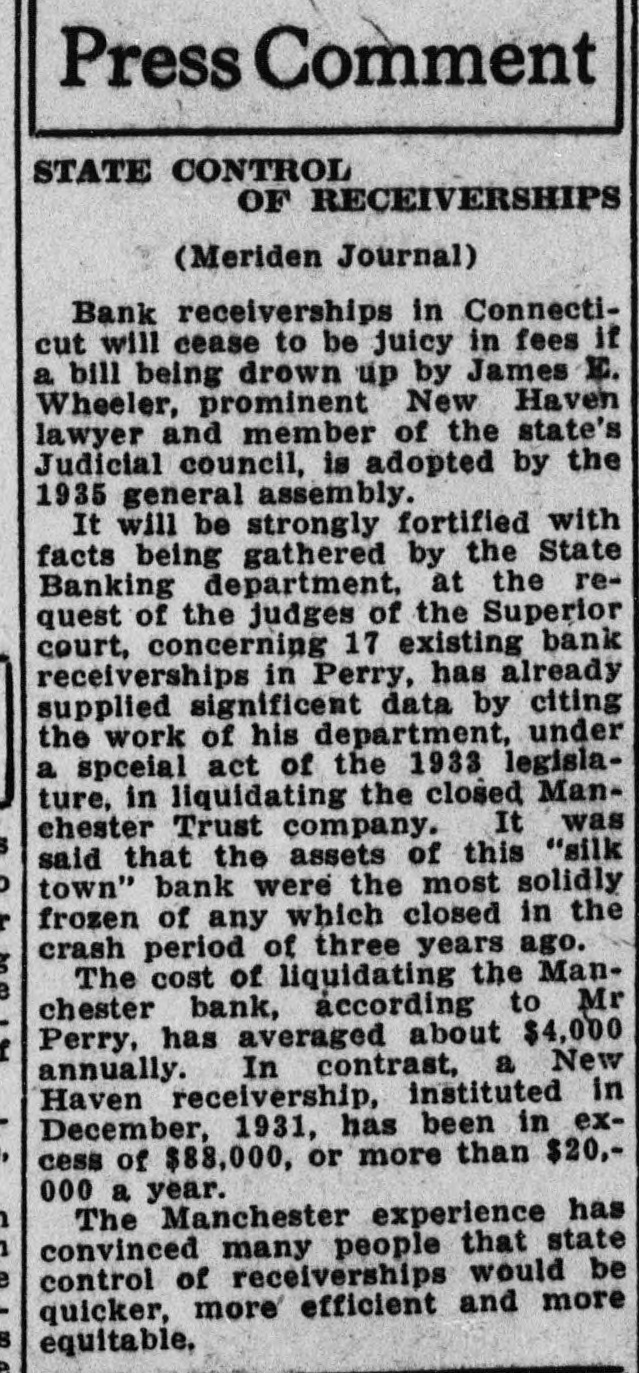

Article Text

Sensing the fact that the Culhane banking bill, as enacted by the General Assembly last week, is loosely drawn, editors of newspapers have given expression to their views on the legislation. The New Britain Herald points to the speed with which the bill was sent through and the Manchester Herald also comments on this. Both papers discuss two different types receiverships from their local viewpoint. The New Britain questions what possible improvement will there be in the New Britain situation because of the new provisions and adds: "Mr. Bassford (receiver for the Commercial Trust Company of New Britain) has given such general satisfaction that any other arrangement will prove obnoxious to depositors." The Manchester Herald recites the satisfactory experience of the Manchester Trust Company depositors the receivership of which was administered by the banking department.

No one objects to enactment of legislation that will make the state banking department the receiver for closed banks, but there is good grounds for fear of legislation containing changes in carefully considered bank regulation, as made in the Culhane bill. The bill passed last week would stand as an example of the poorest bit of legislation passed at this session. Some newspapers have condoned the bill, offering the sop that its faults could be corrected in the future. Endorsement of the Culhane bill, making the bank commissioner receiver for closed banks, was by implication, at least, an expression of confidence in the banking department. That being so, then the expressed opinions of the banking department that the Culhane bill is "unworkable" and probably "unconstitutional," should be heeded and the defects of the bill should be remedied now—not wait two years. The bill, designed, it is claimed, in the interest of depositors, would undoubtedly be the instrument for hindering early liquidation of closed banks. Court procedures can and do tie up and delay business at times.

A fresh start should be made, and this can be accomplished by recall of the Culhane bill, or a veto by the governor.

There have been plenty of insinuations as regard the motives behind the legislation. If there is any ground for the accusations that it is aimed at a particular class it would in itself be good reason for erasure of the bill from the dignity of place among Connecticut statutes.

The New Britain Herald editorial on the receivership bill is reprinted as follows:

"When a bill hits the Legislature suddenly on one day and is passed by both houses the next day, there is cause for suspicion regarding all the hurry—especially at a time when numerous other matters which have been discussed since the beginning of the session still remain on the shelf.

"This refers of course to the new fangled banking bill which will set aside receivers of closed banks and place the banking commissioner in charge. Two years ago a similar idea got no further than a legislative committee.

"Obviously there is good ground for attempting to regulate the banking receiver system, complaint having been widespread that the receivers got too much money for their services, and sometimes the services were of doubtful value. But conditions throughout the state have vastly changed and most of the early receivers of banks which went under during the banking melee have got theirs and have given way to new receivers who get far less and who yield better satisfaction. Such a law would have been valuable three years ago, when in fact it was first suggested.

"The banking commissioner cannot be acting as receiver for many banks at a time. He will need deputy receivers. In the case of the Commercial Trust in New Britain, for instance, this deputy on the ground probably would be Walter Bassford, the present receiver, and speaking of the local situation, what possible improvement will there be possible as a result of the new law? Mr. Bassford has given such general satisfaction that any other arrangement will prove obnoxious to depositors."

The Manchester Herald, also critical of high receivership fees, says in its editorial "the liquidation of the Manchester bank has been conducted by the state bank commissioner without waste and with probably as satisfactory results, considering the plight of the institution when it was closed, as have attended the settlement of any bank's affairs anywhere." The Herald concludes:

"The principle of the Culhane bill is irreproachable. There would seem to be no question at all about bank liquidation being a proper function of the State Banking Department. Whether all the provisions of the new law are wise or not is another matter; there certainly was no adequate time for either the Legislature or the people to inform themselves between the bill's appearance and its passage. But if the act shall turn out to have bad features, features that must be changed at another session, the fault cannot be laid at the doors of the Senator who drew the bill nor the members who passed it, but at that of the Judiciary Committee which failed to bring out a mandatory measure but attempted to pass off on the state a receivership bill which dodged the issue."

Home Insurance Company stock is now being traded ex dividend, declaration of the $1 a share having been voted last Friday. The date of payment has not yet been announced. Wilfred Kurth, president, has announced that the capital increase and transfer authorized by stockholders in connection with the deal with Home Fire Security Corporation, has been completed.

A new tax levy of 2 per cent on fire insurance premiums has been passed by the state assembly of Nebraska, but Governor Cochran is considering a veto. In that connection he is holding conferences. The bill is designed for "firemen's relief." Arguments against the signing of the bill have been made on the ground that mutual companies will have to increase their rates and it is urged upon the governor that the firemen are now protected by compensation laws and pension funds. It is also argued that the tax would be illegal since it was not for a public purpose; also that it discriminates between insured and uninsured properties all of which benefit from services of the firemen.

Biltmore Hotel Corporation has insured its 800 employees under a cooperative group policy amounting in the aggregate to $2,000,000. The policy placed with Equitable Life covers life, accident and and health and accidental death and dismemberment. The group life certificates range from $500 to $5000, according to individual earnings.

New paid-for business, including annuities, placed with the Equitable Life Insurance Co. during April was the largest for the month in the history of the company, totaling $8,404,610, an increase of $3,600,000, or 76.1 per cent over the same month last year. Total paid-for business during the first four months this year amounted to $29,162,994, an increase of $9,920,839, or 51.6 per cent over the like period last year.